Climate Bonds’ Market Intelligence today reveals Green, Social, Sustainability, Sustainability-linked and transition bond (GSS+) reached collective volumes of USD863.4bn in 2022. Volumes fell year-on-year for the first time in a decade as a tough macroeconomic terrain scuppered global bond issuance across the board. Despite this, GSS+ volumes held their 5% share of the global bond market.

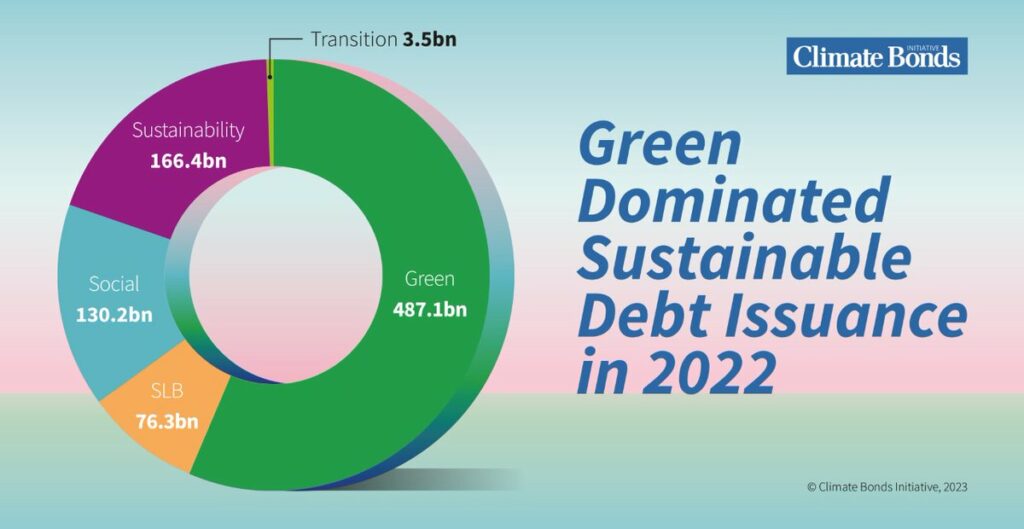

Green bond issuance made up just over half of labelled volumes in 2022, with a USD487.1bn total. Sustainability bonds contributed USD166.4bn, social bonds totaled USD130.2bn, SLBs saw USD76.3bn volumes, whilst transition bonds saw just USD3.5bn. The USD863.4bn total 2022 brings lifetime GSS+ volumes to USD3.7tn by the end of 2022.

The year-on-year growth of GSS+ debt had maintained for over a decade and culminated in a record 2021, in which volumes topped $1trillion and green bonds alone reached USD522.7bn. However, lenders were left reluctant to lock-in high-credit rates as the fixed-income landscape shifted, squeezing supply that historically has been outstripped by heavy investor demand.

Climate Bonds screens self-labelled bonds issued globally and only includes bond issuance demonstrating climate ambition aligned with the Paris Agreement in its Green Bond Database.

Sean Kidney, CEO of Climate Bonds: “Climate change is not about gently rising sea levels; as emissions go up heat, storms, floods get more extreme – the age of volatility has begun. Volatility will give us social and economic disruption, pandemics, wars; the last three years on repeat. We are making progress: half the world’s bond-issuing countries are now issuing green bonds to finance climate action; and strong 2030-focussed action is finally being taken by the US, the EU, India, China and Japan. We expect 2023 to be a stellar year for both green bond issuance and for climate action on the ground.”

5 things not to miss from 2023

- Rigour in the SLB market– SLB’s have soared to over half a trillion issued since market inception only a few years ago. Though, SLB’s have become popular as they offer investors real impact on climate performance at the company level, the varying levels of ambition have been of concern. Climate Bonds’ coming expansion of its Standard and Certification Scheme to SLBs in early 2023 seeks to redress this issue. These efforts will provide rigour in the market, and signal to prospective investors and regulators SLBs that meet best practice against an international recognised standard.

- Rise of Resilience Investments – More than USD2tn of green bonds have been issued to date and this number has the potential to grow to our target of USD5trn of per year by 2025. Demand far outstripping supply remains a key obstacle to reaching this target. There is a tremendous opportunity to tap this demand by scaling-up capital flows towards investments in resilience.

- Government support for green finance – Global policymakers are awakening climate considerations must take centre stage as the world recovers from the pandemic and soaring inflation. Climate forecasting group, Inevitable Policy Response (IPR) calculates the combined total of public money now available in the US for clean energy and climate investment via the Inflation Reduction Act (IRA), Infrastructure and Investment Jobs Act (IIJA) and the CHIPS & Science Act is nearly $1 trillion. Across the Atlantic, Europe is responding with EU Commission President Ursula von der Leyen announcing ‘Green Deal Industrial Plan’ at Davos, which includes the Net Zero Industry Act. The aim is to increase funding of clean energy technologies.

- Transition Bond Tipping Point – It is hoped that 2023 can bring forth a transition tipping point, a much-needed moment for greening the hard-to-abate sectors and aligning heavy industry with global efforts towards net-zero. The nascent transition bond market has trailed in volumes when compared to other labels but there are signs of change. Climate Bonds is developing its own transition standards to help these efforts and inform future frameworks. The announcement expected early in 2023 will complement the coming SLB standards.

- Sovereign issuance steaming ahead – At the end of 2022, Climate Bonds had recorded GSS+ bonds from 43 sovereigns with combined volumes of USD323.7bn. This momentum is expected to continue into 2023 with Israel and India already coming to market with green bonds. Could the market hit 50 sovereign issuing nations by the end of 2023? We think so