Green financing by world’s climate-committed banks is growing quickly Corporate Knights, in partnership with The Banker, releases the 2nd annual Sustainable Banking League Table, which finds a 55% increase in banks’ 2022 outstanding sustainable book compared to 2021. Dutch Triodos Bank ranks third and ING 11th.

The Sustainable Banking League Table evaluates members of the NetZero Banking Alliance (NZBA) that also report under the Task Force on Climate-Related Financial Disclosures (TCFD). A total of 114 banks were eligible in 2023, an increase from 91 in 2022. These banks collectively earned more than US$53 billion in sustainable revenues from their loan books, investment portfolios and underwriting and advisory services in 2022.

In 2022, the total outstanding sustainable loan book for the banks was nearly US$1.1 trillion, a 55% increase from 2021. While this is a step in the right direction, the 2023 Banking on Climate Chaos Report indicates that the 60 largest banks in the world have issued more than US$2.1 trillion in new loans to the fossil fuel industry between 2019 and 2022.

The total sustainable bond underwriting and sustainable project advisory volume among the NZBA-TCFD banks increased 144% to nearly US$1.5 trillion from 2021 to 2022. The increase in these sustainable totals is attributable to a number of factors, including an increased number of banks in the universe, and a significant improvement around sustainable finance disclosure.

Top Performers

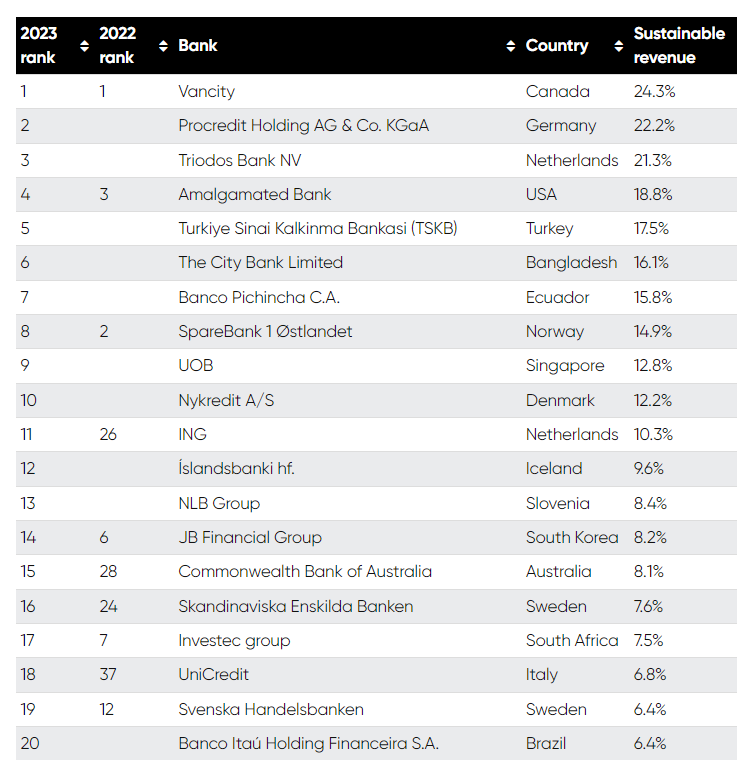

Vancity, which earns significant sustainable revenue via loan support to borrowers from high-emitting sectors to improve emissions measurement and reporting practices, as well as developing climate transition plans, takes the top spot in the ranking for the second year in a row. The bank’s sustainable

revenue ratio decreased to 24.3% in 2022 from 34.1% in 2021.

Amalgamated Bank, which has a sustainable revenue ratio of 18.8%, dropped to fourth from third in the 2023 league table. It earns sustainable revenue from interest on a significant portion (36.5%) of its outstanding loan book dedicated to the category of Climate Protection.

Three newcomers ranked in the Top 5 in the 2023 edition of the Sustainable Banking League Table: ProCredit Holding AG (22.2% SR ratio), Triodos Bank (21.3% SR ratio) and Turkiye Sinai Kalkinma Bankasi (TSKB) (17.5% SR ratio). Third-overall-ranked Triodos Bank, which was part of the universe for the 2022 league table but did not rank due to issues around disclosure, is an ethical bank that markets itself as a leading expert in sustainable banking. In 2022, it reported US$123 million (27.7% of its loan book) in lending in the following sectors that align with the CK SET: organic farming/food; sustainable property; renewable energy and environmental technology.

Second-ranked ProCredit Holding is a recent signatory to the NZBA that was not included in the inaugural Sustainable Banking League Table published in 2022. It is the parent company of a development-oriented group of commercial banks, where the business model of the group is based on “socially responsible banking.” Its 2022 sustainable revenue figure consists of interest earned on outstanding energy efficiency and renewable energy loans.

The Top 5 is completed by TSKB, which became a member of the NZBA in 2022 and was not included in the inaugural Sustainable Banking League Table. Its 2022 sustainable revenue figure consists of a large amount of renewable energy loans since renewable energy projects account for 91% of its electricity generation loan portfolio.

Nordea had US$17.7 billion in sustainable AUM at the end of 2022 – the largest in the universe. These sustainable investments were calculated by mapping Nordea’s portfolio to the companies on the Corporate Knights “green flag” list, which includes companies that have 20% or more of their revenues deemed sustainable under the CK SET, in addition to not having any “red flags,” which is a list of 25 exclusionary screens tracked by CK.

UniCredit SpA had by far the highest volume of sustainable underwriting and advisory services, totalling US$451 billion. This consisted of a volume of green and sustainable bond underwriting totaling US$111 billion and a green loan underwriting volume totalling US$341 billion.

Big Movers/Losers

Türkiye İş Bankası A.Ş. saw the largest rank improvement from the 2021 to 2022 assessment, moving up 30 places to 27th from 57th. CK was able to quantify revenues from a much larger portion of its loan book in this year’s ranking because of direct engagement from the bank. Its 2022 sustainable revenue figure consists of interest revenue earned from the following loan themes: renewable energy; sustainable agricultural; green vehicles; resource efficiency; green buildings; green mortgages; marine conservation and finance provided to women entrepreneurs.

Despite a slight increase in the total amount of sustainable revenue earned from 2021 to 2022, with a sustainable revenue ratio of 0.1%, Virgin Money UK PLC saw the largest rank decrease, dropping to 79th from 35th.

Methodology

The Sustainable Banking League Table Ranking analyzes the revenue sources of banking institutions that are signatories to the Net Zero Banking Alliance and, in addition, are committed to reporting under the Task Force on Climate-Related Financial Disclosures framework. In particular, it examines the amount and percentage of revenue that is obtained from sustainable sources, as defined by the Corporate Knights press release: 2023 Sustainable Banking League Table 3 Corporate Knights Sustainable Economy Taxonomy (CK SET). The institutions with the greatest percentage of sustainable revenue as a share of their overall revenue are ranked the highest.

Sustainable economy research and media organization Corporate Knights conducted the analysis and measured the revenues each institution earned from sustainable loans, sustainable investments and sustainable bond underwriting and project advisory services during 2022, based on activities defined as sustainable within the Corporate Knights Sustainable Economy Taxonomy. Please see the detailed descriptions of the components’ sustainable revenue calculation below:

- Sustainable revenue from loans is calculated by dividing the total outstanding sustainable loan book by the total outstanding loan book, then multiplying this ratio by the annual loan interest revenue.

- Sustainable revenue from investments is calculated in one of two ways:

- – Sustainable revenue from third-party-managed investments is calculated by dividing the sustainable assets under management of the third party investment portfolio by the total assets under management of the third party investment portfolio, then multiplying this ratio by the annual investment management fee income.

- Sustainable revenue from general account investments is calculated by dividing the sustainable assets under management of the general account investment portfolio by the total assets under management of the general account investment portfolio, then multiplying this ratio by the annual investment interest income.

- Sustainable revenue from the provision of sustainable bond underwriting and advisory services is calculated by applying an industry benchmark fee of 0.37% to the total volume of sustainable bonds underwritten and projects on which advised. This fee proxy of 0.37% is based on research conducted by Corporate Knights. We ask that banks disclose the specific income earned from their sustainable underwriting and advisory activities, but as none currently do, we rely on this proxy to determine a sustainable revenue figure.

A total of 114 bank institutions in total were eligible for analysis. Of these, 26 did not report sufficient data or report their data in a format that enabled Corporate Knights to complete its analysis. Therefore, these banks have been excluded from the ranking. Data was obtained via public disclosures (annual reports, sustainability reports, responsible investing reports, etc.) with some supplementary data provided by banks that responded during the data

verification period.

All banking institutions that were assessed were contacted for verification of the data and given four weeks to respond and provide any data that may not have been captured through public disclosures.