Impact investment is rapidly growing. Why? What are the developments? And how does this business pushes towards the transition to a sustainable and inclusive society? In 6 articles we will highlight the developments, opportunities and risks of Purpose & Impact investment. This is the first article.

Environmental & Social Governance (ESG) information is considered as relevant information by all organizational stakeholders. It’s mainly used for CSR/sustainability measurement purposes for management and for external reporting purposes. Since investors understand that the high rated ESG companies financially outperform their peers and the market, a rapid growth of ESG investments took place. Moreover the ESG investments were booming during the COVID-19 outbreak. Reasons enough to explore the developments, positive and negative sides of ESG investing and the ultimate question: how does a company improve their ESG performance?

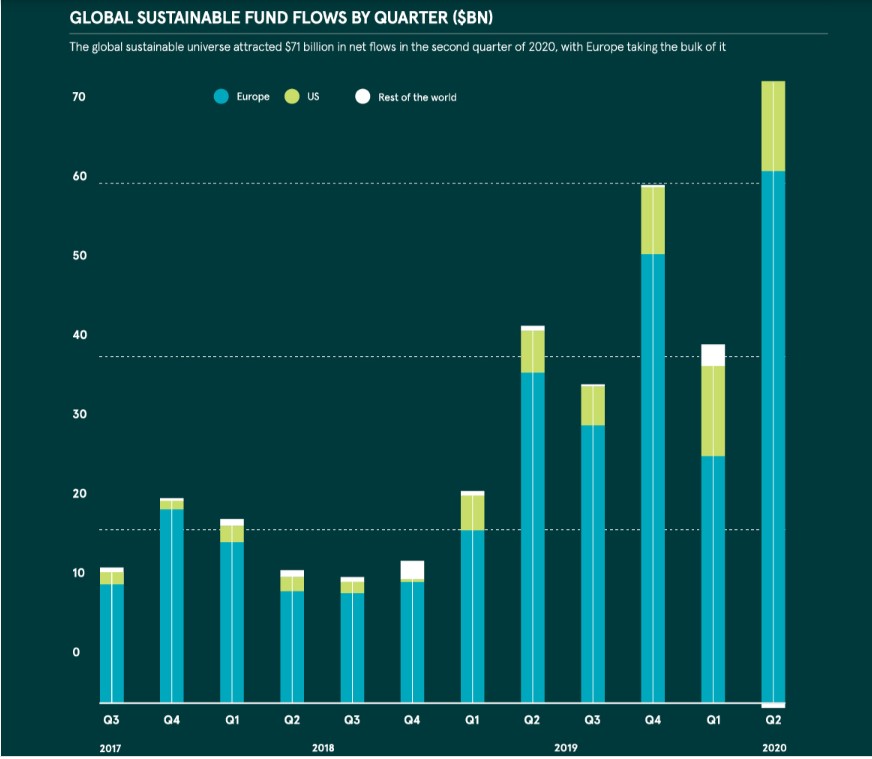

Source: Visual Capitalist August 2020

ESG development

There is hardly any serious institutional investor that wants companies not to be active in ESG. Can you imagine that only ten years ago, this was reversed? General perception was that ESG investments let to lower returns and higher risks. Over the last years this has changed drastically: from a nice to have, to a must have. If a company has no ESG reporting, a growing number of potential investors are not interested. It is not a reward, but a punishment state of mind. Investing in ESG companies and funds (ETF) rapidly evolves as financial performance of these ESG companies and funds are in general outperforming the non ESG ones. As it confirms: there is a causal effect between ESG and financial performance.

The following question emerges: Is an ESG company outperforming the market because they are active in ESG? While there are many researches available about the financial impact of investing in ESG companies, only little academic research can be found on the question why. With a growing knowledge base on ESG investment and shared value creation by companies, it is expected that more models will appear which will show the dependency and interconnections between ESG and other value drivers within a company. Article 6 of this series will explore more on this via Impact Measurement.

What is great about ESG investing?

Do you want to be remembered as company that was doing great by making money? Of by making value? ESG is helping to capture that value by qualifying the efforts, processes and results of a company in a societal context. Consequently, the CEO and the company are rewarded for its ESG progress. Rewarded due to the societal impact of a more ESG operating form, due to financial outperformance and due to the attraction of responsible ESG investors.

ESG investing also pushes companies to raise the bar in terms of quality, transparency and reporting. As a first step, environmental and social figures and targets must be reported. Internal processes must be created and to set up a governance structure. Based on externally available information, investors and other relevant stakeholders could ask questions and engage with the Board on ESG. This mix of visibility and engagement can only let to improvement. In practice we see great examples of how companies make this happen, such as the reduction of carbon emissions: A few years ago, a reduction of CO2 (in line with the Paris agreement) was seen as ambitious. Nowadays this ambition should be carbon neutral or even negative. The disclosure of ESG information on carbon emissions helped.

What is wrong about ESG investing?

ESG investing leads to a better financial return and a better world. How can this be wrong? The vast majority of institutional investors are considering ESG in their decisions and signed up for the Principles for Responsible Investment. Resulting in the fact that almost all public companies are publishing ESG data and work with well-known rating agencies (e.g. MSCI, Bloomberg, ISS, Morningstar, Vigeo Eiris, RobecoSAM, CDP, Thomas Reuters, and more…) to obtain an ESG rating. Consequently the best performing ESG companies per industry are popular amongst the investors and with that also the effect on our planet and it’s life. In theory.

In practice ESG information and intelligence has not the maturity level such as financial data. This is the major concern of investors. And it should, as only a few companies have solid data of ESG performance over the years. And that’s peculiar as we have seen that ESG performance of a company has become one of the most important drivers for investment decisions.

Secondly many companies treat relevant ESG information as a compliance checkbox. Once a year, during the set-up of the annual report, the ESG information is collected and the ESG table is created. So instead of using ESG on a daily basis, integrated in a companies’ strategy and operations, as a way to build a sustainable resilient business, it’s merely to please investors and to get a higher rating.

In addition, there are many companies which draw a better picture of their performance. On purpose. External validation of ESG data has often ‘limited assurance’, meaning the accountant couldn’t find evidence that the reporting data is not true. While for financial data, large team of external verifiers are used, for ESG data, this is very limited. So, plenty of space for ‘ESG washing’. More on this in article 3 of this series: ‘SDG washing’.

Fourth, investors rely on rating agencies, which have an assessment function but do not show the true impact of real performance: An analyst creates a datafile of a company, completes the information and uses big data assumptions to fill the gaps and identify the outliners. On high level this works fine, but zooming in shows two major issues:

- The ESG rating per rating agency can be very different as a recent study from Harvard shows.

- Investment decisions are made based on high-level assumptions, possible wrong, big data.

We believe that solving the issues are related to improving the qualitative ESG data and with that, ESG performance as a first step which we discuss below. And quantifying ESG data which we refer to as Impact Measurement is the second step, which we will discuss in article 6 of this series.

How do we improve ESG performance?

The quality of financial and related commercial business data is needed for the ESG data as well. Meaning that a strong uptake of solid data must occur, over time, just like financial and commercial data. It requires not just an investment in data capturing. It requires a cultural change. People are used to think and act with money, but need to think and act on qualitative ESG data. This is also where a huge opportunity lies. Getting not only the management, but the whole company on board requires a company change. ESG (or internal CSR-sustainability or even impactful purpose) should be in the core of the strategy and vision. Translated to product design and operations. Managed with internal teams and data-systems lead to internal insights and progress, which is part of recurring Board report and discussion. A company which understood this well is SAP.

As a company is in ‘business while being under construction’ there are ways to improve even in short term the ESG performance. But there is no ‘one size fits all’, it’s very company depended. For example the system legacy, which data is tracked, in which detail and by which company entity? What are the processes for capturing and validation data? If a company is just starting, an outside inside view can be helpful: what kind of information the rating agencies are asking? How does this fits our ESG-strategy? Which ESG information is actually relevant? How do we combine ESG information with SDG reports? How does our information fit into ESG ratings? How do we include this information in our annual report? And how are our ESG risks managed, which requires a strong collaboration on risk management (article 2 of this series, will explains the importance and difficulty of this).

ESG investment is here to stay. And companies should aim to not only be the ESG leader of their industry in order to be more attractive for investors, but also to financial outperform the market and to create the societal value of a company. Really “doing well by doing good” (Benjamin Franklin).

About the authors:

Martin de Jong is founder of Empact, impact consultancy and working for (international) clients on Societal Strategy, ESG and Impact Valuation. He is former director Societal Value VodafoneZiggo and Sustainable Business Manager Vodafone PLC. He is lecturer on various universities on sustainable business.

Anne Rademaker is founder of Rademaker Consulting and working with strategic partners (both public and private) to accelerate the transition to a global circular economy. Anne is working with Martin for Empacts ESG & Impact clients. She is a former Senior Consultant at EY with extensive knowledge on Finance, Risk and Process management.

More info on Empact.