Bron

ECB

The euro’s international role remained overall stable in 2019. This was one of the principal findings in the latest annual report on The international role of the euro, published today by the European Central Bank (ECB).

Adjusting for exchange rate valuation effects, the share of the euro in outstanding international loans was 1 percentage point higher at the end of 2019 than at the end of 2018, at 15.4%. The share of the euro in outstanding international debt securities declined. The share of the euro in global foreign exchange reserves and in outstanding international deposits remained broadly stable, as did the share of the euro as an invoicing currency for extra-euro area transactions in goods and the stock of euro banknotes circulating outside the euro area.

Since its introduction 20 years ago, the euro has remained unchallenged as second most used currency globally after the US dollar, but its usage declined after the global financial crisis, bottoming out in 2016. The international role of the euro is primarily supported by a deeper and more complete Economic and Monetary Union (EMU), including advancing the capital markets union, in the context of the pursuit of sound economic policies in the euro area.

“The recent COVID-19 pandemic underlines the urgency of these policies and reform efforts, which are paramount to raising the attractiveness of the euro globally”, said ECB President Christine Lagarde.

The role of the euro in global green bond markets

The report also contains a box on the role of the euro in global green bond markets, with the euro being the main currency of denomination for the issuance of green bonds in 2019. “The swift implementation of an EU taxonomy of sustainable economic activities would provide a credible and standardised framework, ensure greater investor confidence and could thereby also contribute to strengthening the international role of the euro”, said Fabio Panetta, member of the ECB’s Executive Board.

A green bond is a type of fixed-income security whose proceeds are earmarked to finance investment projects with an environmental benefit. These debt instruments are increasingly used by companies, governments and financial institutions to finance the adoption of more energy-efficient technologies, reduce carbon emissions and reorient business models towards sustainable economic activities. While the global green bond market is still relatively small, it has been growing rapidly in recent years. Global green bond issuance was only USD 9.1 billion or 0.2% of total bond issuance in 2014; that figure grew to approximately USD 205 billion or 2.85% of total issuance by 2019. This amounts to a 20 fold increase in the last five years. Growing investor demand for green financial products and the recent entry of sovereign issuers in the market suggest that there is significant potential for further growth in this segment.

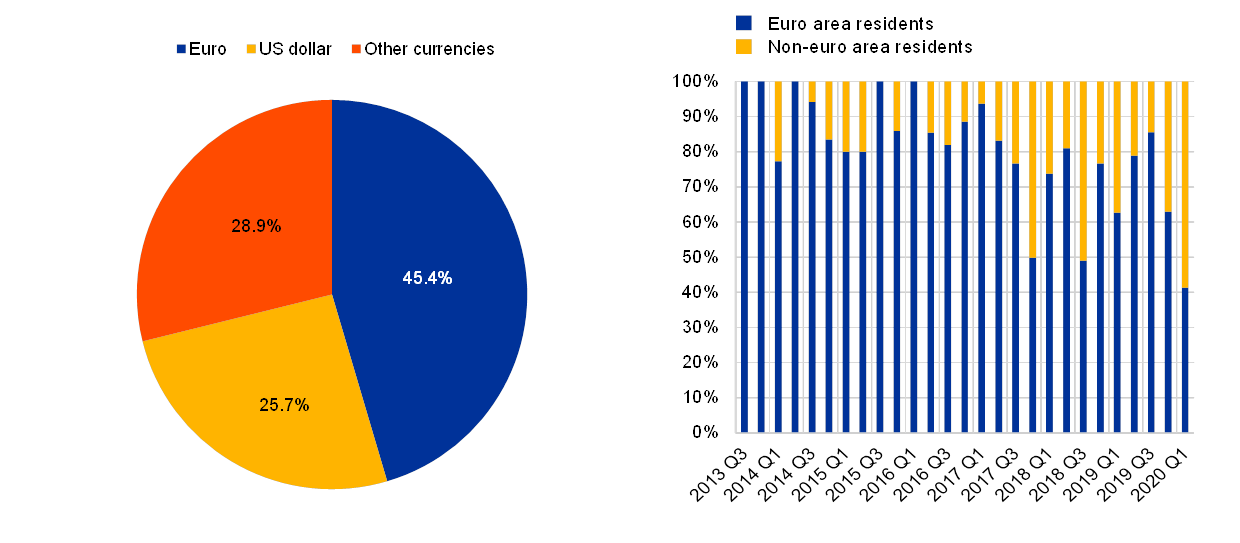

EU residents are the largest issuers of green bonds. In 2019 more than half of global issuance was concentrated in the EU and almost half of global green bond issuance was denominated in euro (see left panel of Chart A). The euro is also leading in terms of relative importance of green bonds compared to other bonds: the proportion of green bonds relative to total bond issuance denominated in euro rose to almost 9% by the end of 2019, compared to 2.1% for bonds in US dollars and around 2.5% for bonds in other currencies. The leading role of the euro does not simply reflect the prevalence of green bond issuers based in the euro area. As shown in the right panel of Chart A, issuance of euro-denominated green bonds is also strong among non-euro area residents, with non-euro area issuers accounting for almost 30% of total euro-denominated green bond issuance in 2019, which suggests that the euro is also attractive for foreign issuers. While incumbent currencies display a significant degree of inertia in established markets, the emergence of new segments of capital markets could provide a window of opportunity for other currencies to gain international use. As the euro is already the main currency of denomination for the issuance of green bonds, the consolidation of the EU role as a global hub for green finance could strengthen the euro as the currency of choice for sustainable financial products, bolstering its international role.

Chart A

Almost half of global green bond issuance is denominated in euro; issuance of euro-denominated green bonds – breakdown by issuer residence

Currency breakdown of green bond issuance in 2019 (left panel) and developments of the share of euro area and non-euro area issuers of green bonds in euro (right panel)

(percentages)

Sources: Dealogic and ECB calculations.

Note: last observation 31 January 2020.

Future developments will depend on multiple factors, including the EU’s ability to fully reap the benefits of the capital markets union and the rapid developments in the regulatory environment. The European Commission launched an Action plan on sustainable finance in 2018. The objective of this action plan was to create an enabling framework for sustainable finance notably through the development of a taxonomy of sustainable economic activities aimed at preventing “greenwashing”, commonly defined as the practice of making an unsubstantiated or misleading claim about the environmental benefits of a financial product.

The swift implementation of the taxonomy could be conducive to strengthening the international role of the euro by providing a credible and standardised framework and ensuring greater investor confidence. Further EU initiatives are ongoing to increase the availability of information on sustainability, develop an EU green bond standard, and enhance international coordination. Whether the euro will benefit from these efforts will also depend on the approaches of other jurisdictions. A number of countries, most notably the United Kingdom, China and Singapore, have also developed green finance strategies to promote the growth of this segment and foster their role as international centres for green finance. One challenge going forward is to avoid regulatory competition undermining efforts to set common standards and to prevent “greenwashing”, which could lead to undue market fragmentation and reduce the environmental benefits of green finance.

Prepared by Lena Boneva and Fabio Tamburrini