Bron

Ceres

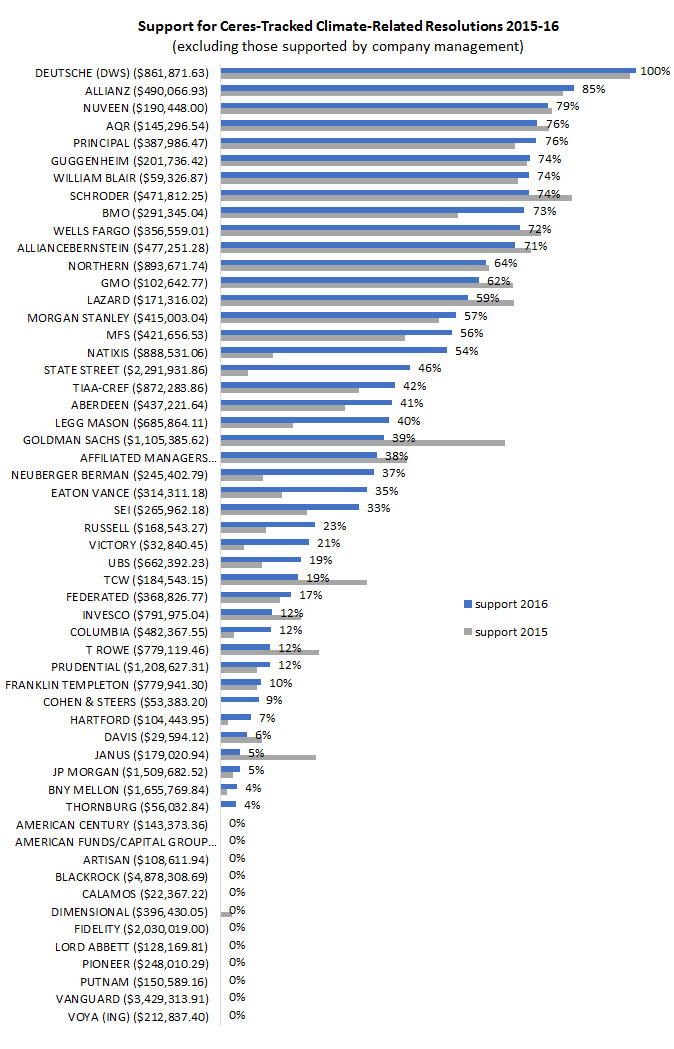

The vast majority of climate scientists (97 percent) believe climate change is real, but what about your mutual fund company? Ceres examined how the US largest mutual fund companies voted on climate-related shareholder resolutions in 2015 and 2016. The results are revealing.

While the great majority of mutual fund companies voted in favor of many climate-related resolutions (as shown on the chart below), a number of the largest firms failed to support any of the resolutions, including big-name players such as American Funds, BlackRock, Dimensional, Fidelity, Pioneer, Putnam, and Vanguard. These firms collectively manage trillions of dollars in assets, and their support of climate resolutions could contribute to majority votes for some resolutions – resulting in enormous pressure on companies to disclose their plans for addressing wide-ranging climate-related risks.

Let’s review why institutional investors file these resolutions and why companies should be disclosing and addressing climate-related risks. First, climate change creates profound risks for many companies and the global economy, and these risks need to be disclosed by companies, as a task force (chaired by Michael Bloomberg) of the Financial Stability Board of the G20 summarizes here.

Second, virtually every country in the world has agreed to reduce climate-warming pollution significantly via the Paris Climate Agreement that formally entered into force in November. The transition to clean energy that is already well underway threatens conventional business models of fossil fuel producers like ExxonMobil and creates a substantial risk of stranded assets and devaluation. Simply put, the business case for companies to disclose and act on climate risks – whether from extreme weather and other physical risks, or carbon-reducing regulatory risks – is powerful.

So why would a mutual fund company vote against nearly every shareholder resolution asking companies to disclose their risks and strategies for dealing with these powerful trends?

Here we explore three possible explanations – none of them are good:

- The fund firm’s leaders don’t believe climate change is real or are ideologically opposed to admitting it’s real. If your mutual fund company falls in this category, you have a problem because the firm’s leaders are either not paying attention, or they are letting incorrect information guide their investment decisions and ownership practices. Either way, you should probably run for the exit.

- They accept the science of climate change, but see few material risks or implications for businesses in their portfolios. This explanation may seem similar to the first, but there is a difference here that may be tripping up these firms. Vanguard’s proxy voting policies (see part five) state that Vanguard funds should abstain from voting on “philosophical” social issues because they are the purview of company management, unless they have a significant impact on the valuation of the business; and based on Vanguard’s voting record, it seems they believe climate change has no significant financial impact on companies.Unfortunately, this logic is both deeply flawed and shortsighted. Yes, climate change is clearly a moral and political issue, but it is also a critical business issue. Coal producers, oil companies and other fossil fuel businesses face wide-ranging climate risks – regulatory risks, transitional/competitive risks and reputational risks, among them. Businesses across nearly all sectors are increasingly exposed to risks of supply chain and workforce disruptions, infrastructure damage, rising resource costs, shifting demand, brand damage, and stronger regulations intended to protect people and the planet for both today and the future. Vanguard has a legal duty to vote in the best interests of its clients, and in our opinion, they are violating that duty by failing to recognize these risks as demonstrated by their failure to vote for a single climate-related resolution tracked by our study. If Vanguard believes climate change is not a business issue simply because it’s also a moral issue, you have to wonder about their judgment.

- The fund firm managers believe private dialogue with companies is a more effective strategy than proxy voting. While it is true that face-to-face discussions initiated by major investors can have a strong influence on companies, it does not remove the fiduciary duty to vote proxies conscientiously on important bottom-line issues. If you believe the company should do what the resolution asks, and you vote against it (or similar requests) year after year while engaging in dialogue about it, then you send a mixed message. Proxy votes by major shareholders can be very effective in moving companies to action.

In addition, many institutional investors engage with companies on resolutions while also voting for them. Voting arguably adds teeth to the negotiations. And mutual fund companies generally keep their dialogues with companies strictly confidential, so there is no way for investors to understand their approach or any possible results.

Now the big kicker.

Vanguard and many other mutual fund firms and investment managers – including American Funds, BlackRock, Dimensional, Fidelity and Lord Abbett – that fail to support climate resolutions have publicly stated that environmental and social issues can be material financially. They are all members of the UN’s Principles for Responsible Investment and have publicly pledged to adhere to six principles. Principle 3 specifically reads: “We will seek appropriate disclosure on environmental, social and governance (ESG) issues by the entities in which we invest.” Many of the resolutions Vanguard and others vote against request this disclosure. And BlackRock and BNY Mellon have publicly issued noteworthy papers and letters to companies on the significant investment implications of climate change.

This proxy voting inconsistency has led investors to file resolutions on the issue with mutual fund companies and investment managers. As Timothy Smith, Senior Vice President of Walden Asset Management, explained: “The proxy voting records on climate change of investment firms and mutual funds are under increasing scrutiny by investors and clients. As a result, investors have filed a resolution with 5 investment firms urging them to review their proxy voting policies and record, as some vote against virtually every social and environmental shareholder resolution.”

Smith continues: “It is troubling to see BlackRock, JP Morgan, BNY Mellon and others routinely vote against important shareholder resolutions seeking reasonable disclosure and goals to manage climate change. How is this consistent with their fiduciary duty to protect their clients interests?”

Customers who are concerned by these poor voting practices should contact their mutual fund companies and suggest that they vote for reasonable climate-related resolutions. Resolutions filed during the 2011 – 2017 proxy seasons are available at www.ceres.org/resolutions, and more are expected to be filed in the coming months for the 2017 season. Much is at stake, in part because an increasing number of these resolutions are receiving strong support (in the 30-40 percent range), and giant mutual fund companies can help push these votes above 50 percent, sending a powerful message to companies that stronger climate risk disclosure and action are an imperative.